Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

What is WACC, its formula, and why it's used in corporate finance

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

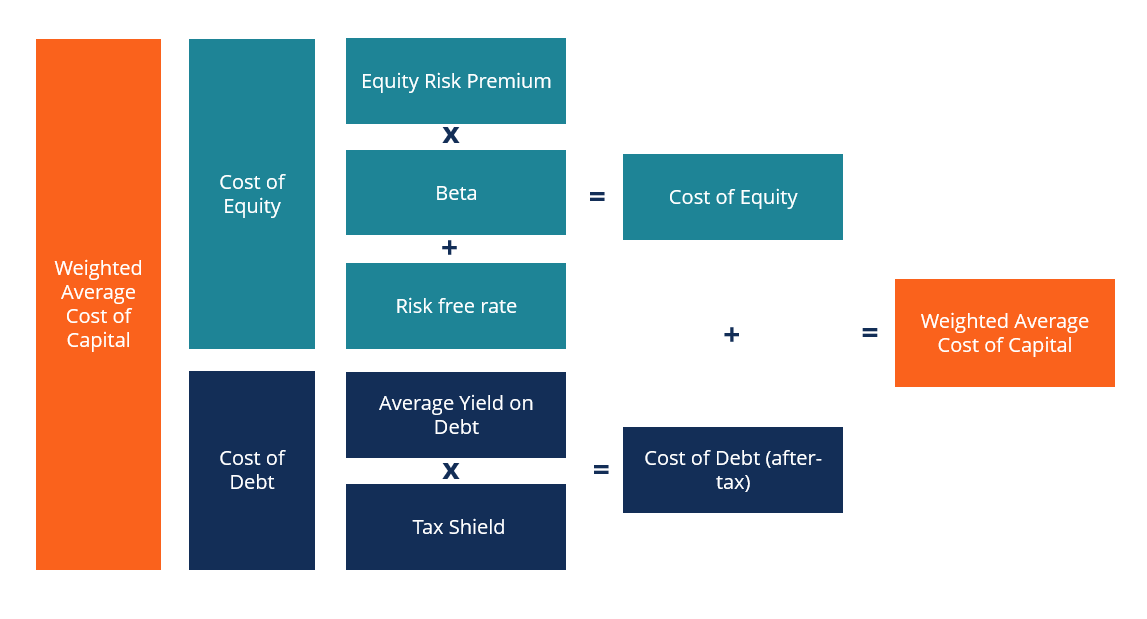

A firm’s Weighted Average Cost of Capital (WACC) represents its blended cost of capital across all sources, including common shares, preferred shares, and debt. The cost of each type of capital is weighted by its percentage of total capital and then are all added together. This guide will provide a detailed breakdown of what WACC is, why it is used, and how to calculate it.

WACC is used in financial modeling as the discount rate to calculate the net present value of a business. More specifically, WACC is the discount rate used when valuing a business or project using the unlevered free cash flow approach. Another way of thinking about WACC is that it is the required rate an investor needs in order to consider investing in the business.

Learn more: CFI’s Business Valuation Resources.

As shown below, the WACC formula is:

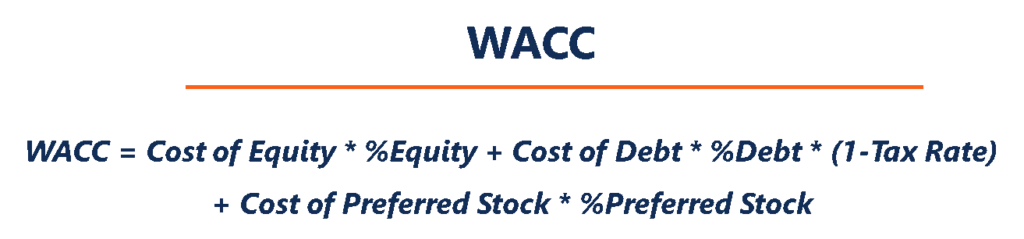

WACC = (E/V x Re) + ((D/V x Rd) x (1 – T))

Where:

E = market value of the firm’s equity (market cap)

D = market value of the firm’s debt

V = total value of capital (equity plus debt)

E/V = percentage of capital that is equity

D/V = percentage of capital that is debt

Re = cost of equity (required rate of return)

Rd = cost of debt (yield to maturity on existing debt)

T = tax rate

An extended version of the WACC formula is shown below, which includes the cost of preferred stock (for companies that have preferred stock).

The purpose of WACC is to determine the cost of each part of the company’s capital structure based on the proportion of equity, debt and preferred stock it has. Each component has a cost to the company. The company usually pays a fixed rate of interest on its debt and usually a fixed dividend on its preferred stock. Even though a firm does not pay a fixed rate of return on common equity, it does often pay cash dividends.

The weighted average cost of capital is an integral part of a DCF valuation model and, thus, it is an important concept to understand for finance professionals, especially for investment banking, equity research and corporate development roles. This article will go through each component of the WACC calculation.

The cost of equity is calculated using the Capital Asset Pricing Model (CAPM) which equates rates of return to volatility (risk vs reward). Below is the formula for the cost of equity:

Re = Rf + β × (Rm − Rf)

Where:

Rf = the risk-free rate (typically the 10-year U.S. Treasury bond yield)

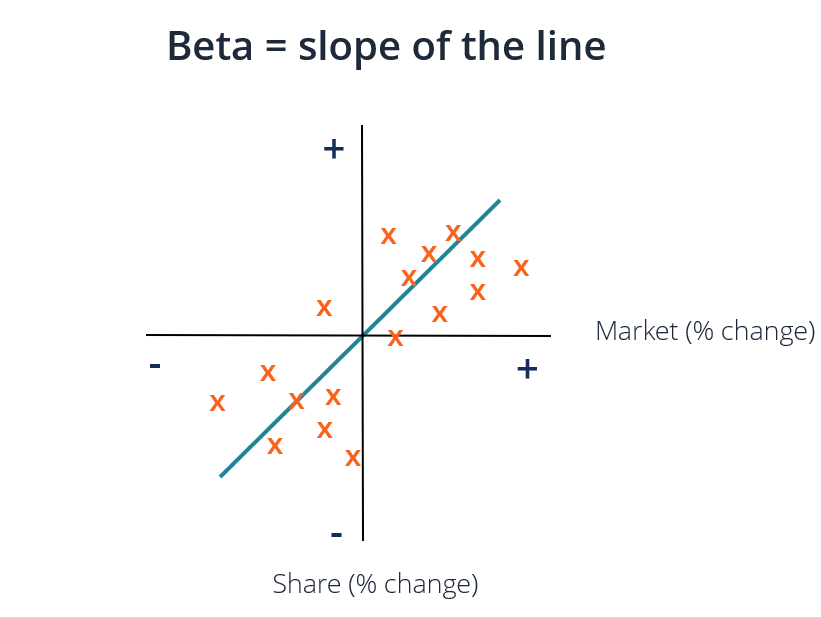

β = equity beta (also known as the levered beta)

Rm = annual return of the stock market

The cost of equity is an implied cost or an opportunity cost of capital. It is the rate of return an investor requires in order to compensate for the risk of investing in the stock. Beta is a measure of a stock’s volatility of returns relative to the overall stock market (often proxied by a large stock index like the S&P 500 index). If you have the data in Excel, beta can be easily calculated using the SLOPE function. See below for more on beta.

The risk-free rate is the return that can be earned by investing in a risk-free security, e.g., U.S. Treasury bonds. Typically, the yield of the 10-year U.S. Treasury is used for the risk-free rate. It’s called risk free because it is free from default risk; however, other risks like interest rate risk still apply.

The equity risk premium (ERP) is defined as the extra yield that can be earned over the risk-free rate by investing in the stock market. One simple way to estimate ERP is to subtract the risk-free return from the market return. This information will normally be enough for most basic financial analysis. However, estimating the ERP can be a much more detailed task in practice. Generally, banks take the ERP from publications by Morningstar or Kroll (formerly known as Duff and Phelps).

Beta refers to the volatility or riskiness of a stock relative to all other stocks in the market. There are a couple of ways to estimate the beta of a stock. The first and simplest way is to calculate the company’s historical beta (using regression analysis). Alternatively, there are several financial data services that publish betas for companies.

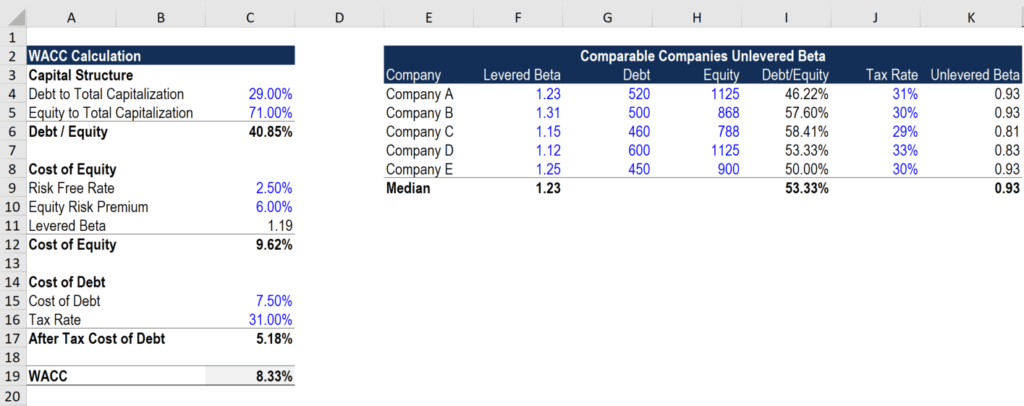

The second, and more thorough, approach is to make a new estimate for a company’s beta using public company comparables. To use this approach, the beta of comparable companies is taken from one of the financial data services. Then the unlevered beta for each company is calculated using the following formula:

Unlevered Beta = Levered Beta / ((1 + (1 – Tax Rate) * (Debt / Equity))

The levered beta includes both business risk and the risk that comes from taking on debt. However, since different firms have different capital structures, the unlevered beta (also known as the asset beta) is calculated to remove additional risk from debt in order to view pure business risk. The average of the unlevered betas is then calculated and re-levered based on the capital structure of the company that is being valued:

Levered Beta = Unlevered Beta * ((1 + (1 – Tax Rate) * (Debt / Equity))

In most cases, the firm’s current capital structure is used when beta is re-levered. However, if there is information that the firm’s capital structure might change in the future, then beta would be re-levered using the firm’s target capital structure.

After calculating the risk-free rate, equity risk premium, and levered beta, the cost of equity = risk-free rate + equity risk premium * levered beta.

Learn more: CFI’s Business Valuation Resources.

Determining the cost of debt and preferred stock is probably the easiest part of the WACC calculation. The cost of debt is the yield to maturity on the firm’s debt. Similarly, the cost of preferred stock is the dividend yield on the company’s preferred stock. Simply multiply the cost of debt and the yield on preferred stock with the proportion of debt and preferred stock in a company’s capital structure, respectively.

Since interest payments are tax-deductible, the cost of debt needs to be multiplied by (1 – tax rate), which is referred to as the value of the tax shield. This is not done for preferred stock because preferred dividends are paid with after-tax profits.

Take the weighted average current yield to maturity of all outstanding debt then multiply it one minus the tax rate and you have the after-tax cost of debt to be used in the WACC formula.

Learn the details in CFI’s Math for Corporate Finance Course.

Below is a screenshot of CFI’s WACC Calculator in Excel, which you can download for free in the form below.

Enter your name and email in the form below and download the free template now!

The Weighted Average Cost of Capital serves as the discount rate for calculating the value of a business. It is also used to evaluate investment opportunities, as WACC is considered to represent the firm’s opportunity cost of capital. Thus, it is used as a hurdle rate by companies.

A company will commonly use its WACC as the hurdle rate for evaluating mergers and acquisitions (M&A), as well as for financial modeling of internal investments. If an investment opportunity has a lower Internal Rate of Return (IRR) than its WACC, it should not invest in the project and may choose to buy back its own shares or pay out a dividend to shareholders.

Nominal free cash flows (which include inflation) should be discounted by a nominal WACC and real free cash flows (excluding inflation) should be discounted by a real weighted average cost of capital. Nominal is more common in practice, but it’s important to be aware of the difference.

WACC is used as the discount rate when performing a valuation using the unlevered free cash flow (UFCF) approach. Discounting UFCF by WACC derives a company’s implied enterprise value. Equity value can then be be estimated by taking enterprise value and subtracting net debt. To obtain equity value per share, divide equity value by the fully diluted shares outstanding.

Learn more: CFI’s Business Valuation Resources.

Despite it’s prevalence in corporate finance, WACC does have several limitations:

Many professionals and analysts in corporate finance use the weighted average cost of capital in their day-to-day jobs. Some of the main careers that use WACC in their regular financial analysis include:

Learn more about the cost of capital from Kroll.

To keep advancing your career, the additional CFI resources below will be useful: