Seller’s Discretionary Earnings

A cash-flow based measure of business earnings in an owner-operated business

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is Seller’s Discretionary Earnings?

Seller’s discretionary earnings is a cash-flow based measure of business earnings in an owner-operated business. It comprises the profit before tax and interest of a business before the owner’s benefits, non-cash expenses, extraordinary one-time investments, and other non-related business incomes and expenses. This metric is used to measure the value of an organization in order to provide potential buyers with a better picture of their expected return on investment.

From the seller’s side, calculating the seller’s discretionary earnings allows them to maximize the value of the business before getting into a business sale negotiation with potential buyers. Understanding how to calculate the seller’s discretionary earnings allows the seller to make the right decision when choosing what expenses and incomes to include.

To Learn how to perform Valuation Methods such as DCF, Comps and Precedent Transactions, check out CFI’s Business Valuation Modeling Course.

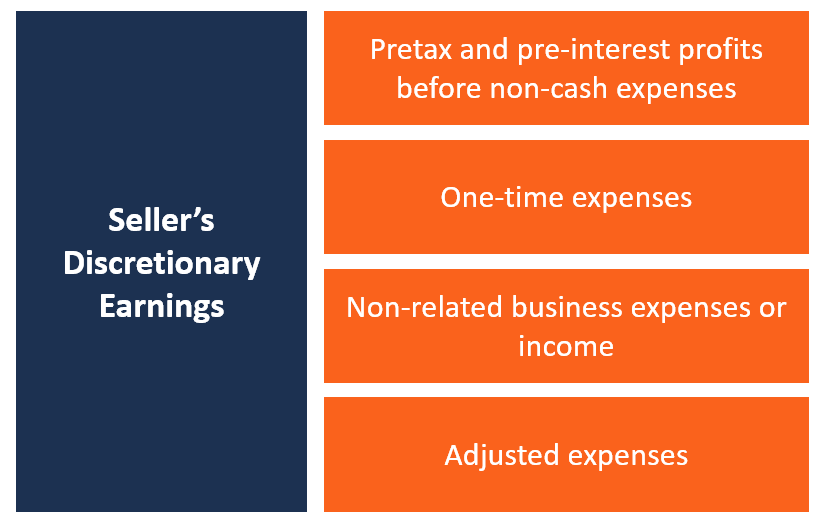

Components of the Seller’s Discretionary Earnings

When preparing a business for sale, there are various incomes and expenses that may or may not have an effect on the company’s valuation. Knowing what to include in the valuation can help both parties in the negotiation process reach a reasonable valuation of the business. Here are some of the items that are included when calculating the seller’s discretionary earnings:

#1 Pretax and pre-interest profits before non-cash expenses

This is the EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization), which shows how much the company is earning. It gives the investor an overview of the return on investment that they will get once they acquire the business.

#2 One-time expenses

One-time purchases include expenses that are non-recurring and are only paid once. The expenses may include payments for website design services, purchase of a business license, one-time application fees, legal fees, etc.

#3 Non-related business expenses or income

This comprises incomes and expenses that are not related to the business’ core operations. Typical non-related incomes and expenses include costs incurred on a business trip for a personal vacation, consulting income not related to the business activities, fuel and automobile expenses for a business that does not require automobiles, and office rent recorded as business expenses.

#4 Adjusted expenses

When selling a business, one must account for some of the expenses that are complementary to that business. For example, when a company is selling its branded t-shirts website, the new owner will need to factor in the expenses for warehouse rent and order fulfillment since they are crucial to the success of the business. Such expenses must be included when preparing the earnings statement for the business.

Areas of Disagreements between Buyers and Sellers

When calculating the seller’s discretionary earnings, there is a likelihood that the seller and the buyer will disagree on some of the incomes, expenses, and replacement costs that should be included in the calculations. The common areas of disagreements include:

#1 One-time expenses

Some of the expenses included under one-time expenses may be disputed by the potential buyer on the basis of whether they are one-time expenses or they will recur in the future. For example, license fees that are included as one-time expenses may need to be paid again in the future.

The same applies to web design fees since the new buyer will need to redesign the website after a few years to update it to the latest technologies. The buyer and the seller will need to agree on the appropriate items to be recorded as one-time expenses.

#2 Replacement owner’s benefits

Another item where the buyer and the seller may disagree is the replacement owner’s benefit. A business may have more than one owner, and this means that the value of the seller’s discretionary earnings may be overstated or understated. If a business has more than one owner earning an income from the business, only one owner’s benefit can be added back to the earnings for valuation purposes.

The other owner’s benefits should be adjusted to represent current market rates that are equal to what the new owner will pay a full-time employee to perform that function. The point of disagreement may be where the owner’s benefit represents reasonable value for the amount of work performed.

Similarities between Seller’s Discretionary Earnings and EBITDA

Both Seller’s Discretionary Earnings and Earnings before Interest, Taxes, Depreciation, and Amortization (EBITDA) attempt to calculate standardized earnings by excluding certain items that are variable from one business to another. For example, both metrics exclude interest expense on debt since each company has different debt levels. Including the expense may bring big variances in reported earnings.

Seller’s discretionary earnings are used when valuing smaller companies, while the EBITDA metric is more commonly used when valuing large companies.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™ certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Free Accounting Courses

Learn accounting fundamentals and how to read financial statements with CFI’s free online accounting classes.

These courses will give the confidence you need to perform world-class financial analyst work. Start now!

Building confidence in your accounting skills is easy with CFI courses! Enroll now for FREE to start advancing your career!