Matching Principle

Reporting expenses at the same time as the related revenues

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is the Matching Principle?

The matching principle is an accounting concept that dictates that companies report expenses at the same time as the revenues they are related to. Revenues and expenses are matched on the income statement for a period of time (e.g., a year, quarter, or month).

Example of the Matching Principle

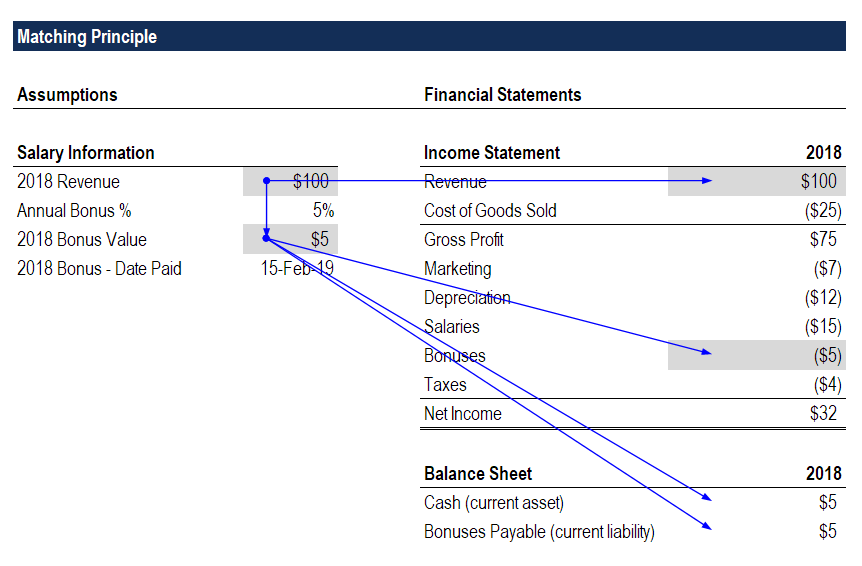

Imagine that a company pays its employees an annual bonus for their work during the fiscal year. The policy is to pay 5% of revenues generated over the year, which is paid out in February of the following year.

In 2018, the company generated revenues of $100 million and thus will pay its employees a bonus of $5 million in February 2019.

Even though the bonus is not paid until the following year, the matching principle stipulates that the expense should be recorded on the 2018 income statement as an expense of $5 million.

On the balance sheet at the end of 2018, a bonuses payable balance of $5 million will be credited, and retained earnings will be reduced by the same amount (lower net income), so the balance sheet will continue to balance.

In February 2019, when the bonus is paid out there is no impact on the income statement. The cash balance on the balance sheet will be credited by $5 million, and the bonuses payable balance will also be debited by $5 million, so the balance sheet will continue to balance.

Download CFI’s Matching Principle template to see how the numbers work on your own!

Benefits of the Matching Principle

The matching principle is a part of the accrual accounting method and presents a more accurate picture of a company’s operations on the income statement.

Investors typically want to see a smooth and normalized income statement where revenues and expenses are tied together, as opposed to being lumpy and disconnected. By matching them together, investors get a better sense of the true economics of the business.

It should be mentioned though that it’s important to look at the cash flow statement in conjunction with the income statement. If, in the example above, the company reported an even bigger accounts payable obligation in February, there might not be enough cash on hand to make the payment. For this reason, investors pay close attention to the company’s cash balance and the timing of its cash flows.

Challenges with the Matching Principle

The principle works well when it’s easy to connect revenues and expenses via a direct cause and effect relationship. There are times, however, when that connection is much less clear, and estimates must be taken.

Imagine, for example, that a company decides to build a new office headquarters that it believes will improve worker productivity. Since there’s no way to directly measure the timing and impact of the new office on revenues, the company will take the useful life of the new office space (measured in years) and depreciate the total cost over that lifetime.

For example, if the office costs $10 million and is expected to last 10 years, the company would allocate $1 million of straight-line depreciation expense per year for 10 years. The expense will continue regardless of whether revenues are generated or not.

Another example would be if a company were to spend $1 million on online marketing (Google AdWords). It may not be able to track the timing of the revenue that comes in, as customers may take months or years to make a purchase. In such a case, the marketing expense would appear on the income statement during the time period the ads are shown, instead of when revenues are received.

Additional resources

Thank you for reading this guide to understanding the accounting concept of the matching principle.

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)T® designation, created to help transform anyone into a world-class financial analyst. To continue learning and advancing your career, these additional CFI resources will be useful:

Free Accounting Courses

Learn accounting fundamentals and how to read financial statements with CFI’s free online accounting classes.

These courses will give the confidence you need to perform world-class financial analyst work. Start now!

Building confidence in your accounting skills is easy with CFI courses! Enroll now for FREE to start advancing your career!