Home Equity Line of Credit (HELOC)

A line of credit with a house as collateral

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is Home Equity Line of Credit (HELOC)?

A Home Equity Line of Credit (HELOC) is a line of credit given to a person using their house as collateral. It is a type of loan in which a bank or financial institution authorizes the borrower to access loan funds as needed, up to a specified maximum amount. Since the collateral is a house, a HELOC is mostly used for large expenditures, such as major home renovations, the purchase of property, payment of medical bills, or education.

Summary

- A home equity line of credit (HELOC) is a loan using a house as collateral.

- As a line of credit, the borrower can use any amount up to the approved maximum.

- There are traditional and hybrid HELOCs. The payment schedule and amount depend on the type.

HELOC vs. Mortgage

The structure of a HELOC is different from a mortgage, but both use a home as collateral. When a person decides to use a mortgage to purchase a house, they get the entire sum of the mortgage up front. On the other hand, a HELOC is more like revolving credit card debt. The person with the HELOC can borrow up to a certain maximum amount at whatever time they choose.

The second difference is the interest rate attached to the loans. For most mortgages, there is a fixed interest rate that is decided at the time the mortgage is signed. For a HELOC, there is usually a floating rate that is based on the prime lending rate. This makes a HELOC riskier as the borrower may have to deal with volatile interest rates. If the prime lending rate suddenly increases, then the borrower will have to shoulder the increased payments.

The third difference is the payment of the loans. For a mortgage, there are fixed interest and principal payments. They are often paid on a monthly basis and are decided when the mortgage is signed. A HELOC only requires interest payments. This, again, is similar to a credit card in which only a minimum payment is required and the principal payments can be pushed back. If a borrower uses $10,000 of the HELOC on a 2% interest rate, the borrower only needs to pay back $200 in interest and not the principal amount of $10,000. The principal is only required at the specified end of the draw period.

Different Types of HELOC

HELOCs are separated into traditional and hybrid categories. A traditional HELOC is as described above. The interest rate is floating and is subject to change, and there are no fixed payment requirements. The requirements for a traditional HELOC are more stringent. They typically enable the homeowner to borrow up to 65% of their home’s value. To qualify for a HELOC, the borrower usually needs to have at least 20% home equity.

A hybrid HELOC allows homeowners to borrow up to 80% of the home’s value. Hybrid HELOCs are more like mortgages, as a portion amortizes, which means it requires payments of both principal and interest.

Traditional HELOCs are considered riskier for lenders. This is due to the fact that borrowers only need to pay the interest payment, which is based on a floating rate. If the interest rate suddenly rises, then homeowners may find themselves in a situation in which they can not make the required payments.

Also, as with a mortgage loan, falling home prices may leave borrowers with “negative equity.” This means they owe more debt on their home than what their property is worth.

HELOC Example

Below is the information for homeowner A:

The appraised home value is $1,250,000. Since the homeowner is applying for a hybrid HELOC, the maximum amount available for the line of credit is 80% of the home value. For this hybrid product, the HELOC portion is 65%, while the amortizing mortgage portion is 15%.

Below is the calculation for Homeowner A’s maximum HELOC credit limit:

The HELOC credit limit can be calculated by taking the maximum amount available for the line of credit and subtracting the outstanding mortgage amount. The HELOC available for Homeowner A is $960,000.

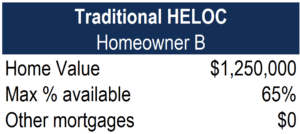

Below is the information for homeowner B:

The appraised home value is $1,250,000, and the homeowner does not have other loans that use the house as collateral. For a traditional HELOC, the maximum amount available is 65% of home value.

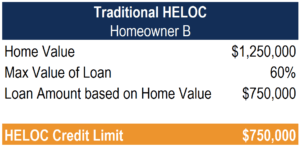

Below is the calculation for Homeowner B’s maximum HELOC credit limit:

To arrive at the HELOC credit limit, multiply the home value with the max value of the loan percentage. Since this homeowner does not have other outstanding loans, the max HELOC limit is $750,000.

Additional Resources

Thank you for reading CFI’s article on the home equity line of credit (HELOC). To keep learning and advancing your career, these additional CFI resources will be helpful: