Get In-Demand Finance Certifications

Audit

An examination of the financial statements of a company

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

What is an Audit?

An audit refers to an examination of the financial statements of a company. Audits are conducted to provide investors and other stakeholders with confidence that a company’s financial reports are accurate. Audits also provide regulators with the assurance that a company is adhering to the appropriate legal and regulatory standards.

It’s easy to think of an audit as a financial investigation, where a company’s financial statements are scrutinized by an external or internal auditor to ensure it is accurate and free of errors. After an audit, the auditor will provide an opinion on whether the financial statements accurately reflect the financial position of the company.

Summary

- An audit is an examination of the financial statements of a company, such as the income statement, cash flow statement, and balance sheet.

- Audits provide investors and regulators with confidence in the accuracy of a corporation’s financial reporting.

- Once completed, the auditor will provide an opinion on whether the financial statements accurately reflect the financial position of the corporation.

How It Works

Although there are many types of audits, in the context of corporate finance, an audit typically refers to those conducted on public or private corporations. Government agencies, such as the Securities and Exchange Commission (SEC), require publicly listed companies to conduct an independent audit to validate their annual financial reporting.

For private companies, audits are not legally required but are still conducted to provide investors, banks, and other stakeholders with confidence in the company’s financial position. During an audit, different financial statements are examined, such as the income statement, cash flow statement, and balance sheet.

The audit provides stakeholders and regulatory agencies with information on how money is earned and spent throughout the fiscal year. Depending on the size of the company, an audit can span a few months to an entire year. At the end of the engagement, the auditor provides a professional opinion on the accuracy of the financial reporting done.

Internal vs. External Audits

Internal audits are performed by employees within the company. The audits tend to focus less on the financial statements, and greater emphasis is placed on a company’s operations and corporate governance.

Internal audit reports are not available to the public but are provided to a company’s executives and audit committee to provide an overview of the organization’s performance across different areas. The areas can include risk management, internal controls, and compliance.

External audits involve independent auditors hired to express an opinion on the accuracy of a corporation’s financial reporting. For public companies, the results of an external audit are reported to the public and are conducted following the Generally Accepted Audit Standards (GAAS).

Most large companies engage with one of the Big Four accounting firms to conduct an audit of their financial statements. To put it into perspective, the Big Four firms audit more than 99% of the S&P 500 companies.

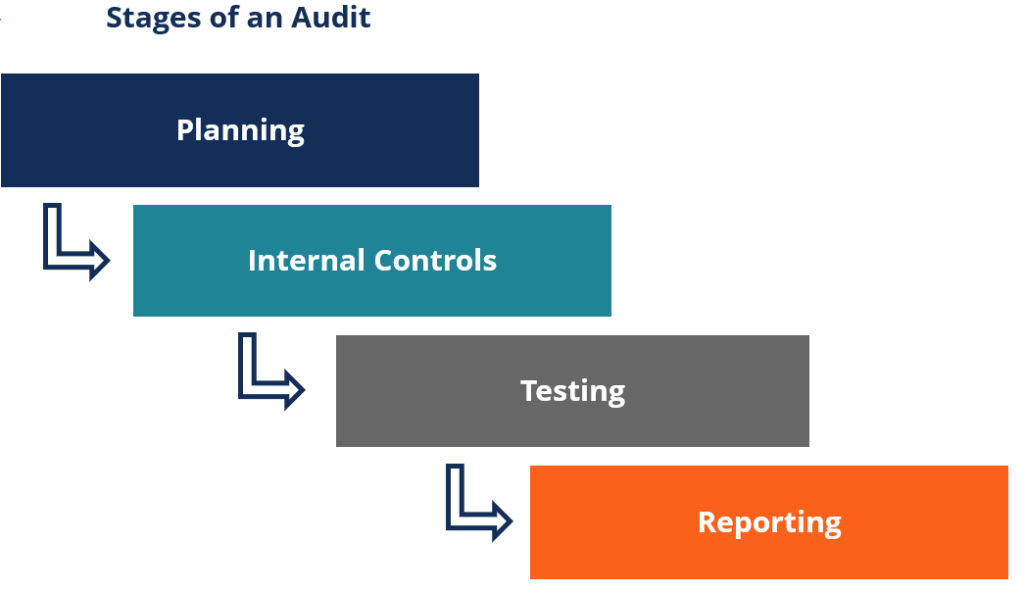

Stages of an Audit

How an audit is conducted can differ depending on the size of the corporation and the complexity of the case. However, an audit usually has four main stages:

- The first stage is the planning stage. In this stage, a corporation engages with the auditing firm to establish details, such as the level of engagement, procedures, and objectives.

- The second stage is the internal controls stage. In this stage, auditors gather financial records and any other information necessary to conduct their audits. The information is necessary to evaluate the accuracy of the financial statements.

- The third stage is the testing stage. In this stage, auditors examine the accuracy of the financial statements using various tests. It may involve verifying transactions, overseeing procedures, or requesting more information.

- The fourth stage is the reporting stage. After completing all the tests, the auditors prepare a report that expresses an opinion on the accuracy of the financial statements.

Levels of Audit Engagement

Many companies choose to engage with internal and external auditors in the preparation of their year-end financial statements. However, the depth of the auditor’s investigation may vary depending on the type of engagement and the assertion level required.

In a full audit engagement, the auditor conducts a complete and thorough investigation of the financial statements, including verifications of income sources and operating expenses. For example, the auditor may compare reported account receivables with receipts from actual customer orders.

At the end of the engagement, the auditor will provide an opinion on the accuracy of the financial statements. A full audit engagement also provides investors, regulators, and other stakeholders with confidence in a corporation’s financial position.

In a review engagement, an auditor only conducts limited examinations to ensure the plausibility of the financial statements. In contrast with an audit, the review engagement only assures that the financial statements are fairly stated, and no further examinations are conducted to verify the accuracy of the statements. Therefore, a review engagement does not provide the same level of confidence in the accuracy of the financial reporting relative to an audit.

In a notice to reader engagement, the role of the auditor is solely to help a company compile its financial information into presentable financial statements. No further examinations are performed, and no opinions are expressed on the accuracy of the financial reporting. Notice to reader engagements is typically only utilized by small corporations without any obligations to external stakeholders.

Additional Resources

Thank you for reading CFI’s guide to Audit. To keep advancing your career, the additional resources below will be useful:

0 search results for ‘’

People also search for:

excel

Free

free courses

accounting

ESG

Balance sheet

wacc

Explore Our Certifications

Resources

Popular Courses

Recent Searches