Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Cost of Goods Sold divided by Inventory

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

The inventory turnover ratio, also known as the stock turnover ratio, is an efficiency ratio that measures how efficiently inventory is managed. The inventory turnover ratio formula is equal to the cost of goods sold divided by total or average inventory to show how many times inventory is “turned” or sold during a period. The ratio can be used to determine if there are excessive inventory levels compared to sales.

The formula for calculating the ratio is as follows:

Where:

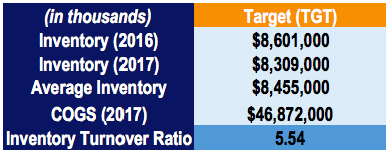

For example, Walmart Inc. (WMT) and Target Corporation reported the following figures in financial statements:

The ratio for Walmart is calculated as follows:

Likewise, the ratio for Target is calculated as follows:

By comparing the inventory turnover ratios of Walmart and Target, two companies that operate mainly in the retail industry, we can see that Walmart sells its inventory 8.26x over a period of one year compared to Target’s 5.54x.

It implies that Walmart can more efficiently sell the inventory it buys. In addition, it may show that Walmart is not overspending on inventory purchases and is not incurring high storage and holding costs compared to Target.

Inventory turnover ratio is an efficiency ratio that measures how well a company can manage its inventory. It is important to achieve a high ratio, as higher turnover rates reduce storage and other holding costs.

It is vital to compare the ratios between companies operating in the same industry and not for companies operating in different industries. The benchmark ratio varies greatly depending on the industry.

A low turnover implies that a company’s sales are poor, it is carrying too much inventory, or experiencing poor inventory management. Unsold inventory can face significant risks from fluctuating market prices and obsolescence.

Depending on the industry that the company operates in, inventory can help determine its liquidity. For example, inventory is one of the biggest assets that retailers report. If a retail company reports a low inventory turnover ratio, the inventory may be obsolete for the company, resulting in lost sales and additional holding costs.

Thank you for reading CFI’s guide to Inventory Turnover Ratio. To keep learning and advancing your career, the following CFI resources will be helpful: