Property and Casualty Insurers

Companies that provide coverage on assets and liability insurance for accidents, injuries, and damage to other people or their belongings

What are Property and Casualty (P&C) Insurers?

Property and casualty (P&C) insurers are companies that provide coverage on assets (e.g., house, car, etc.) and also liability insurance for accidents, injuries, and damage to other people or their belongings.

Summary

- Property and casualty (P&C) insurers are companies that provide coverage on assets, as well as liability insurance for accidents, injuries, and damage to others or their belongings.

- P&C insurers cover a number of things, including auto insurance, home insurance, marine insurance, and professional liability insurance.

- Customers pay P&C insurers an insurance premium for their desired coverage.

Coverage for Property and Casualty Insurers

Outlined in the Canadian Institute of Actuaries, property and casualty insurers focus on risks that result in losses to property and possessions. Examples include:

- Auto insurance: Covering losses to individuals and properties arising from auto accidents and other unforeseen auto events.

- Home insurance: Covering losses to residences and property arising from extreme weather, fire, theft, or other incidents. In addition, covering liability to third parties from actions by the insured.

- Marine insurance: Covering losses to shipping vehicles.

- Professional liability insurance: Covering losses to professional clients arising from negligence.

Scenarios That Property and Casualty Insurers Cover

The following are several scenarios in which property and casualty insurance provide coverage:

1. A visitor fractures their leg on your property due to your negligence

Josh, an insured individual, forgets to shovel his front yard after a snowy day and causes a stranger to fall and fracture their leg. The property and casualty insurer can help John cover the medical costs related to the stranger, as well as damages for pain and suffering.

2. Property is vandalized and damaged

Tim, an insured individual, comes home to find his property vandalized. The property and casualty insurer can help Tim cover the cost related to repairing the damage done to the property.

3. Property is damaged from extreme weather

Dan, an insured individual, lives in Florida, and his property was damaged due to a hurricane recently. The property and casualty insurer can help Dan cover the costs related to damage to the property.

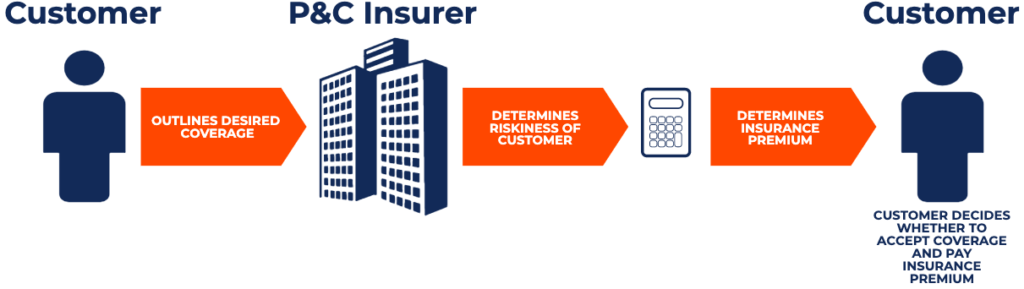

How Does Property and Casualty Insurance Work?

Property and casualty insurers offer insurance to customers for risks, up to a certain coverage amount, in exchange for insurance premiums. Insurance premiums are cash outflows made by the customer in exchange for insurance coverage.

Similar to other insurers, when property and casualty insurers offer coverage to a customer, they must determine an insurance premium the customer will pay by looking at the riskiness of the customer. An insurer would commonly look at the likelihood of the customer making a claim and the potential amount of the claim when calculating the amount of insurance premium they should charge. A diagram is provided below to outline the process:

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: