Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Connecting bank accounts to financial statements

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

A bank reconciliation statement is a document that compares the cash balance on a company’s balance sheet to the corresponding amount on its bank statement. Reconciling the two accounts helps identify whether accounting changes are needed. Bank reconciliations are completed at regular intervals to ensure that the company’s cash records are correct. They also help detect fraud and any cash manipulations.

When banks send companies a bank statement that contains the company’s beginning cash balance, transactions during the period, and ending cash balance, the bank’s ending cash balance and the company’s ending cash balance are almost always different. Some reasons for the difference are:

Nowadays, many companies use specialized accounting software in bank reconciliation to reduce the amount of work and adjustments required and to enable real-time updates.

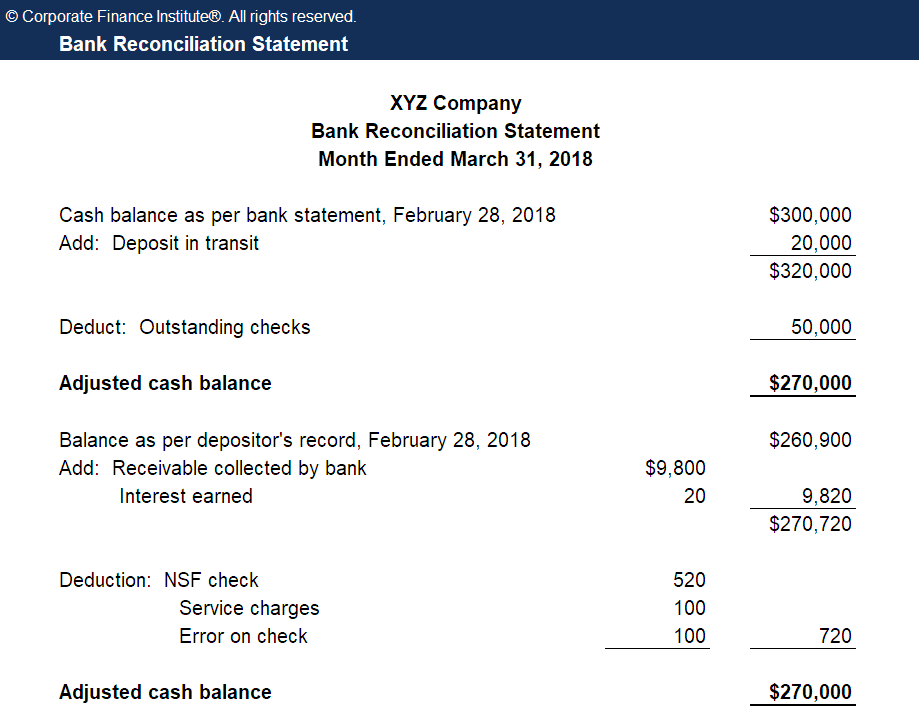

XYZ Company is closing its books and must prepare a bank reconciliation for the following items:

| Amount | Adjustment to Books | |

|---|---|---|

| Ending Bank Balance | $300,000 | |

| Deduct: Uncleared cheques | – $50,000 | None |

| Add: Deposit in transit | + $20,000 | None |

| Adjusted Bank Balance | $270,000 | |

| Ending Book Balance | $260,900 | |

| Deduct: Service charge | – $100 | Debit expense, credit cash |

| Add: Interest income | + $20 | Debit cash, credit interest income |

| Deduct: Error on check | – $100 | Debit expense, credit cash |

| Add: Note receivable | + $9,800 | Debit cash, credit notes receivable |

| Deduct: NSF check | – $520 | Debt accounts receivable, credit cash |

| Adjusted Book Balance | $270,000 |

After recording the journal entries for the company’s book adjustments, a bank reconciliation statement should be produced to reflect all the changes to cash balances for each month. This statement is used by auditors to perform the company’s year-end auditing.

Enter your name and email in the form below and download the free template now!

Download the free Excel template now to advance your finance knowledge!

Below is a video explanation of the bank reconciliation concept and procedure, as well as an example to help you have a better grasp of the calculation of cash balance.

Through financial modeling courses, training, and exercises, anyone in the world can become a great analyst. To keep advancing your career, the additional CFI resources below will be useful: