Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A loan that is secured by an asset

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

Asset-based lending refers to a loan that is secured by an asset. In other words, in asset-based lending, the loan granted by the lender is collateralized with an asset (or assets) of the borrower.

In asset-based lending, the loan is secured by the assets of the borrower. Examples of assets that can be used to secure a loan include accounts receivable, inventory, marketable securities, and property, plant and equipment (PP&E).

As the loan is secured by an asset, asset-based lending is considered less risky compared to unsecured lending (a loan that is not backed by an asset or assets) and, therefore, results in a lower interest rate charged. In addition, the more liquid the asset, the less risky the loan is considered and the lower the interest rate demanded.

For example, an asset-based loan secured by accounts receivable would be deemed safer than an asset-based loan secured by a property – the property is illiquid, and the creditor might find it difficult to liquidate the asset on the market quickly.

Asset-based lending commonly references the loan-to-value ratio. For example, a lender may state “the loan-to-value ratio for this asset-based loan is 80% of marketable securities.” It states that the lender would only be willing to provide a loan of up to 80% of the value of the marketable securities.

The loan-to-value ratio depends on the type of asset – lenders are generally willing to offer a higher loan-to-value ratio for more liquid assets. The loan-to-value ratio is calculated as follows:

Where:

Generally, the loan-to-value ratios for receivables and inventories are 70% and 50%, respectively.

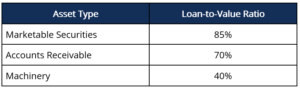

A lender offers the following loan-to-value ratios for certain assets:

A borrower requires a $100,000 loan and owns the following assets:

If the borrower is only able to use one asset to secure the loan, which asset should the borrower use to secure a loan of at least $100,000?

The borrower should use machinery to secure the maximum loan.

Asset-based lending offers the following advantages to the borrower:

Asset-based lending provides the following advantages for the lender:

CFI has a new course on Asset-based Lending and Alternative Finance, an elective course in CFI’s CBCA® Program that compares types of alternative lending structures, including Asset-based lending (ABL) lines. Also, see all our commercial lending resources.