Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Market for raising equity capital and trading financial instruments

The equity capital market is a subset of the broader capital market, where financial institutions and companies interact to trade financial instruments and raise capital for companies. Equity capital markets are riskier than debt markets and, thus, also provide potentially higher returns.

Equity capital is raised by selling a part of a claim/right to a company’s assets in exchange for money. Thus, the value of the company’s current assets and business define the value of its equity capital. The following instruments are traded on the equity capital market:

Common stock shares represent ownership capital, and holders of common shares/stock are paid dividends out of the company’s profits. Common shareholders have a residual claim to the company’s income and assets. They are entitled to a claim in the company’s profits only after the preferred shareholders and bondholders have been paid.

The earnings available to common shareholders (EAS) are given by the following formula:

Earnings Available to Shareholders (EAS) = Profit after Tax – Preferred Dividend

Note: Profit after Tax = Operating profits (/Earnings before Interest and Tax) – Tax

The variability in the returns of shareholders depends on the company’s debt-to-equity ratio. The higher the proportion of debt financing, the fewer the number of shares with claims to the company’s profits. If the profits exceed the interest payments, the excess profit is distributed to shareholders. However, if the interest payments exceed the profits, the loss is distributed to shareholders. The higher the debt-to-equity ratio, the higher will be the variability in the payment of dividends (and vice versa).

However, common shareholders have no legal right to be paid a dividend. Thus, the dividend paid depends on the discretion of management. Similarly, in the event of liquidation, the shareholder’s claim to the company’s asset ranks after that of creditors and preferred shareholders. Thus, common shareholders face a higher degree of risk than other creditors of the company but also have the prospect of higher returns.

Preferred shares are a hybrid security because they combine some features of debentures and common equity stock. They are like debentures because they have a fixed/stated rate of dividends, have a claim to the company’s income and assets before equity, do not have a claim in the company’s residual income/assets, and do not confer voting rights to shareholders.

However, just like a common equity dividend, preferred dividends are not tax-deductible. The various types of preferred shares are irredeemable preferred shares, redeemable preferred shares, cumulative preferred shares, non-cumulative preferred shares, participating preferred shares, convertible preferred shares, and stepped preferred shares.

Equity investments made through private placements are known as private equity. Private equity is raised by private limited enterprises and partnerships, as they cannot trade their shares publicly. Typically, start-up and/or small/medium-sized companies raise capital through this route from institutional investors and/or wealthy individuals because:

An ADR is a certificate of ownership issued in the name of a foreign company by an American bank, against the foreign shares deposited in the bank by the said foreign company. The certificates are tradeable and represent ownership of shares in a foreign company.

ADRs promote the trading of foreign shares in America by admitting the shares of foreign companies into a well-developed stocked market. They often represent a combination of many foreign shares (for instance, lots of 100 shares). ADRs and their associated dividends are denominated in US dollars.

Global depository receipts (GDRs) are negotiable receipts that are issued against the shares of foreign companies by financial institutions situated in developed countries.

A futures contract is a forward contract traded on an organized exchange. They are entered into and executed through clearinghouses. Thus, clearinghouses act as intermediaries between the buyer and seller of the futures contract. The clearinghouse also guarantees that both parties adhere to the contract.

A one-sided contract, an option provides one party with the right but not the obligation to sell or buy the underlying asset on or before a pre-determined date. To acquire this right, a premium is paid. An option to buy is known as a call option, while an option that confers the right to sell is known as a put option.

A swap is a transaction under which one stream of cash flow is exchanged for another between two parties.

The equity capital market acts as a platform for the following functions:

Large-cap, mid-cap, and small-cap companies can be listed on the equity capital market. Investment bankers, retail investors, venture capitalists, angel investors, and securities firms are the dominant traders on the ECM.

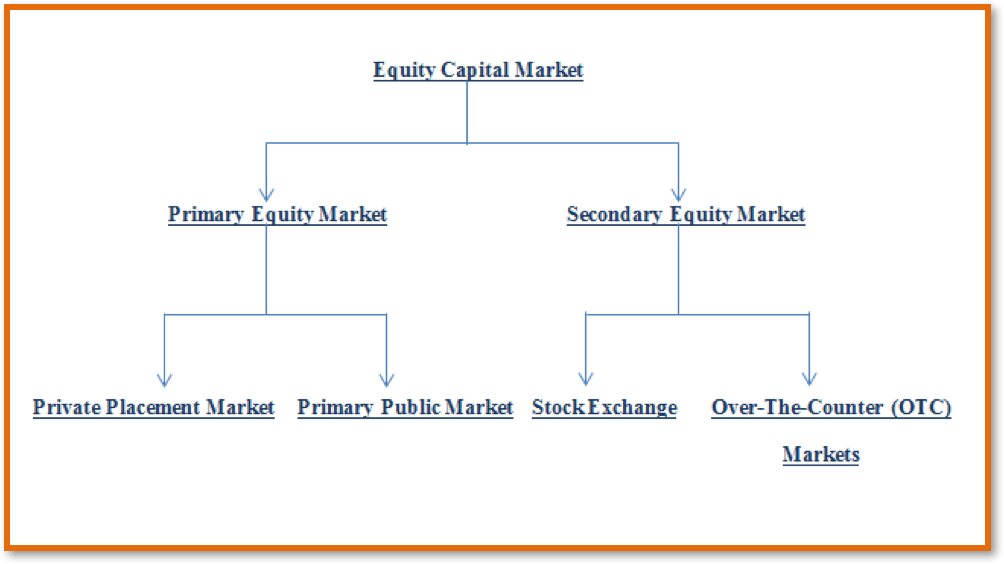

The equity capital market can be divided into two parts:

Allows companies to raise capital from the market for the first time. It is further divided into two parts:

The private placement market allows companies to raise private equity through unquoted shares. It provides a platform where companies can sell their securities to investors directly. In this market, companies do not need to register securities with the Securities and Exchange Commission (SEC), as they are not subject to the same regulatory requirements as listed securities. Typically, the private placement market is illiquid and risky. As a result, investors in this market demand a premium as compensation for their risk-taking and the lack of liquidity in the market.

The primary public market deals with two activities:

When a firm issues stock on the stock exchange, it may do so without creating new shares, i.e., it may exchange unquoted stock for quoted stock. In such a case, the initial investor receives the proceeds earned by selling the newly quoted shares.

However, if the company creates new shares for the issue, the proceeds from the sale of those shares are credited to the company. Furthermore, investment banks are major players in the primary public market because both IPOs and SEOs/SPOs require their underwriting services.

The secondary equity market provides a platform for the sale and purchase of existing shares. No new capital is created in the secondary equity market. The holder of the security, and not the issuer of the traded security, receives proceeds from the sale of the security in question. The secondary equity market can be further divided into two parts:

A stock exchange is a central trading location where the shares of companies listed on the stock exchange are traded. Each stock exchange has its own criteria for listing a company on its exchange. The most commonly used criteria are:

The OTC market is a network of dealers who facilitate the trading of stocks bilaterally between two parties without a stock exchange acting as an intermediary. The OTC markets are not centralized and organized. Thus, they are easier to manipulate than stock exchanges.

Raising capital in the equity market provides a company with the following advantages:

A company faces the following disadvantages by raising capital in the equity market:

Private Equity in China – Process, Opportunities and Challenges