Marginal Tax Rate

A rate charged on taxable income for every extra dollar earned as income

What is the Marginal Tax Rate?

The marginal tax rate is the rate charged on taxable income for every additional dollar earned. It is a federal tax system known as a progressive tax. The progressive tax system uses a structure in which individuals with higher taxable income pay more in taxes, while those in the lower tax bracket pay less. The system uses different tax rates at each tax bracket.

Summary

- The marginal tax rate is a rate charged on taxable income for every additional dollar earned.

- It is a progressive tax system where individuals who earn more pay more taxes, while those in the lower income tax bracket pay less.

- U.S. marginal tax rates are spread into seven tax brackets and grouped into four taxable households.

Understanding Marginal Tax Rate

Historically, taxpayers are subdivided into seven tax brackets and spread across four households. The marginal tax rate system increases as an individual’s income moves higher in the tax bracket scale. It means that a lower taxable dollar earning will be charged at a lower marginal tax rate.

As the taxable income increases to the next tax bracket, it is charged at a higher rate. The rate increases progressively until the last dollar’s highest marginal tax rate.

Taxable Income Practical Example

Let’s say John’s total income per annum is $75,000. However, he places a claim for individual deductions like retirement contributions, Health Saving Accounts (HSA), and student loan interest.

His taxable income will be the income after the refundable deductions. If the total deductions amounted to $12,000, his taxable income will be $63,000 ($75,000 – $12,000).

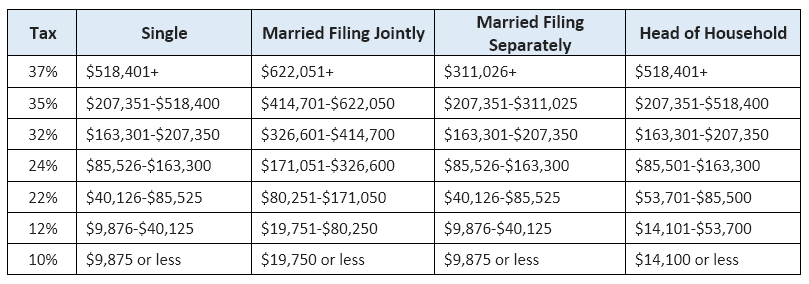

The Federal Tax Brackets and Rates For 2021

The federal tax brackets and rates are different marginal tax rates charged across the seven tax brackets. They are provided and updated by the International Revenue Service (IRS). To standardize them, IRS reviews them annually to account for inflation.

The table below shows the 2020/2021 federal income tax brackets across the four types of households:

How to Calculate the Marginal Tax Rate

When calculating the marginal tax rate, the lowest taxable income bracket is charged at the lowest marginal rate. The remaining taxable income fills the next bracket and is charged at the next marginal tax rate until it is exhausted in the maximum tax bracket.

One concern that many people have is the additional tax liability that arises when their income slides into the next tax bracket. The general misconception is that they will incur heavy taxes due to the higher tax rate. However, only the extra portion of income that slides into the upper tax bracket is taxed.

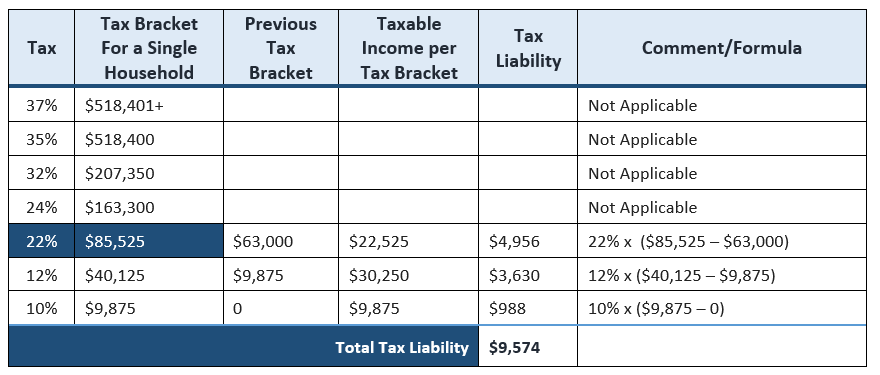

Practical Example 1

Continuing with the example of a total taxable income of $63,000, here is how to calculate John’s annual tax if he will be filing taxes for a single household.

According to the federal income tax and rates, with a taxable income of $63,000, John’s taxable income will fall within the tax bracket with an income of $85,525, which comes with a tax rate of 22%. It means his total tax liability will be $9,574.

Practical Example 2

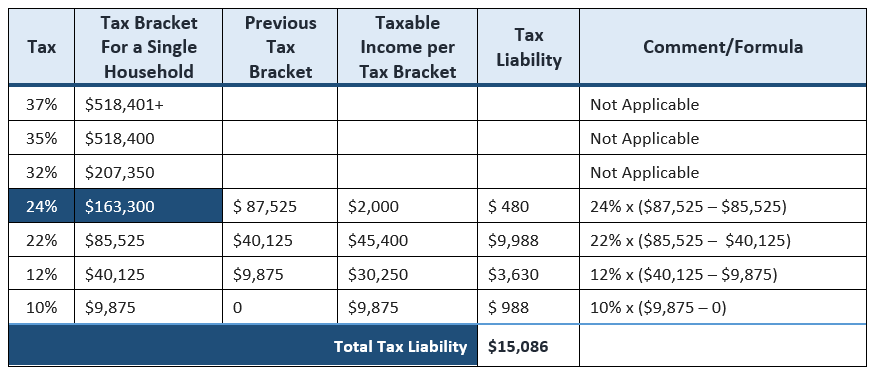

Let’s say John is planning to carry a project that will potentially increase his taxable income to the next tax bracket of $163,300, which is charged at the marginal tax rate of 24%. He is projecting his taxable income will increase to $87,525 from $63,000. The table below shows how John should determine his tax liability to inform his investment decision.

By increasing his taxable income by $24,525, John’s tax liability will increase by $5,512 or 57.6% from $9,574. However, he will have increased his net income by 33.7% ($19,013).

Marginal Tax Rate vs. Effective Tax Rate

From the practical example above, the total tax due was $9,574. When you divide the tax payable with the taxable income of $63,000 and multiply by 100, you get 15.2%. The resultant percentage is called the effective tax rate.

Effective Tax Rate = [$9,574 (Tax Payable) / $63,000 (Taxable Income)] * 100 = 15.2%

Marginal Tax Rate vs. Flat Tax Rate

The flat tax rate is a predetermined fixed percentage taxed to all people regardless of their income level. For example, for a taxable income of $63,000 taxed at a flat tax rate of 15%, John is liable to a total of $9,450 in taxes.

Most economists view, flat rate taxes as an oppressive system to the people in the lower-income levels because they are taxed at the same rate as individuals with high income. Regardless, some states in the United States, such as New Hampshire, Michigan, Tennessee, Colorado, Indiana, Pennsylvania, Illinois, and Massachusetts, use a flat tax rate system.

Related Readings

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: