Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Holding a long position in the underlying asset and purchasing a put option on it

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

A protective put is a risk management and options strategy that involves holding a long position in the underlying asset (e.g., stock) and purchasing a put option with a strike price equal or close to the current price of the underlying asset. A protective put strategy is also known as a synthetic call.

A protective put strategy is analogous to the nature of insurance. The main goal of a protective put is to limit potential losses that may result from an unexpected price drop of the underlying asset.

Adopting such a strategy does not put an absolute limit on potential profits of the investor. Profits from the strategy are determined by the growth potential of the underlying asset. However, a portion of the profits is reduced by the premium paid for the put.

On the other hand, the protective put strategy does create a limit for potential maximum loss, as any losses in the long stock position below the strike price of the put option will be compensated by profits in the option. A protective put strategy is typically employed by bullish investors who want to hedge their long positions in the asset.

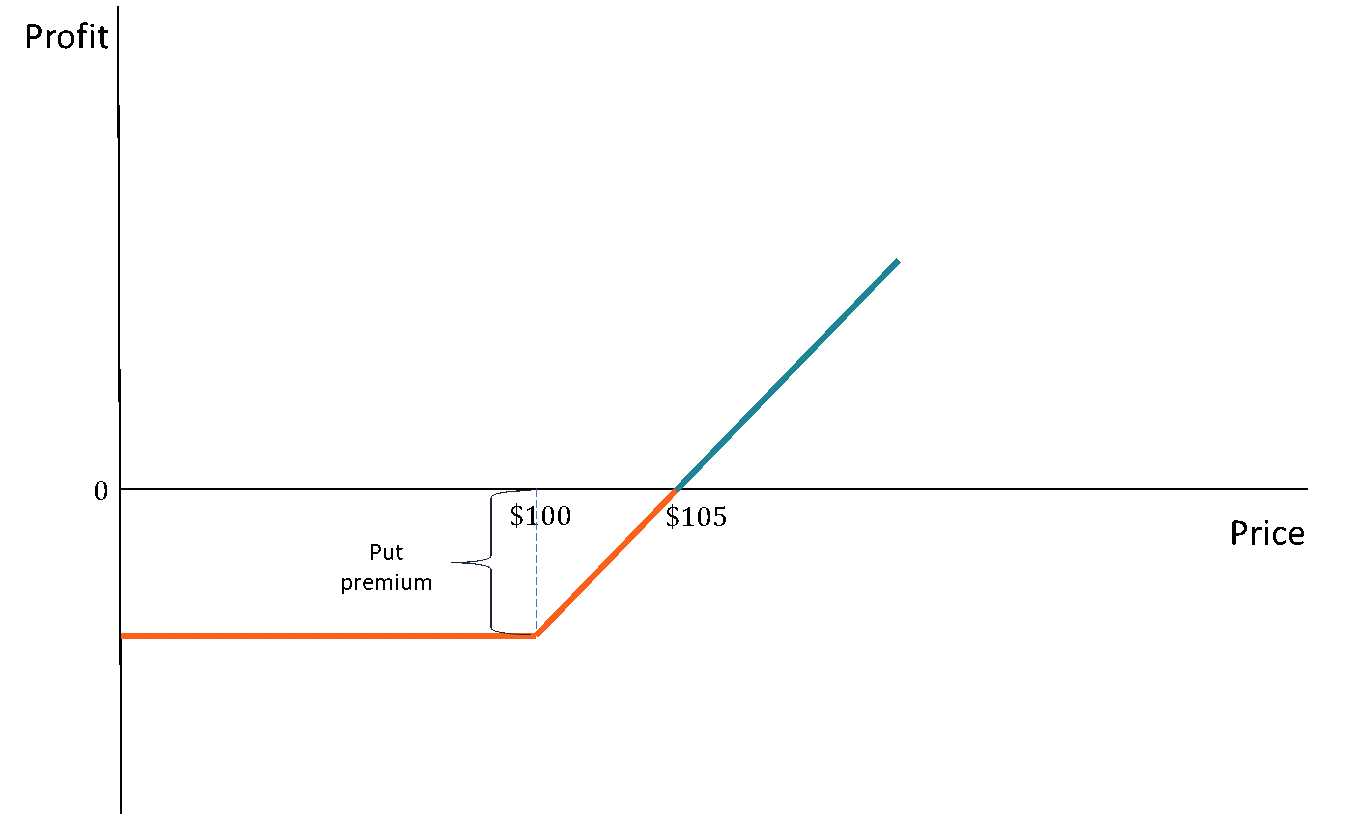

You own 100 shares in ABC Corp, with each share valued at $100. You believe that the price of your shares will increase in the future. However, you want to hedge against the risk of an unexpected price decline. Therefore, you decide to purchase one protective put contract (one put contract contains 100 shares) with a strike price of $100. The premium of the protective put is $5.

The payoff from the protective put depends on the future price of the company’s shares. The following scenarios are possible:

Scenario 1: Share price above $105.

If the share price goes beyond $105, you will experience an unrealized gain. The profit can be calculated as Current Share Price – $105 (it includes initial share price plus put premium). The put will not be exercised.

Scenario 2: Share price between $100 and $105.

In this scenario, the share price will remain the same or slightly rise. However, you will still lose money or hit the breakeven point in the best case. The small loss is caused by the premium you paid for the put contract. Similar to the previous scenario, the put will not be exercised.

Scenario 3: Share price below $100.

In this case, you will exercise the protective put option to limit the losses. After the put is exercised, you will sell your 100 shares at $100. Thus, your loss will be limited to the premium paid for the protective put.

Thank you for reading CFI’s guide on Protective Put. To keep learning and advancing your career, the additional resources below will be useful: