Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The different types of security instruments used by venture capital firms when investing in early stage companies

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets.

Venture capital financing is a type of private equity investing specific to earlier-stage businesses that require capital. In return, the investor receives an equity stake in the business through the issuance of some type of security instrument.

Venture capital firms have a variety of different securities they use depending on the nature of the investment. The most common securities are convertible debt (often called convertible debentures), SAFE notes, and preferred stock.

The kind of instrument an investor chooses depends on a variety of factors related to the company and the investor’s own risk tolerance.

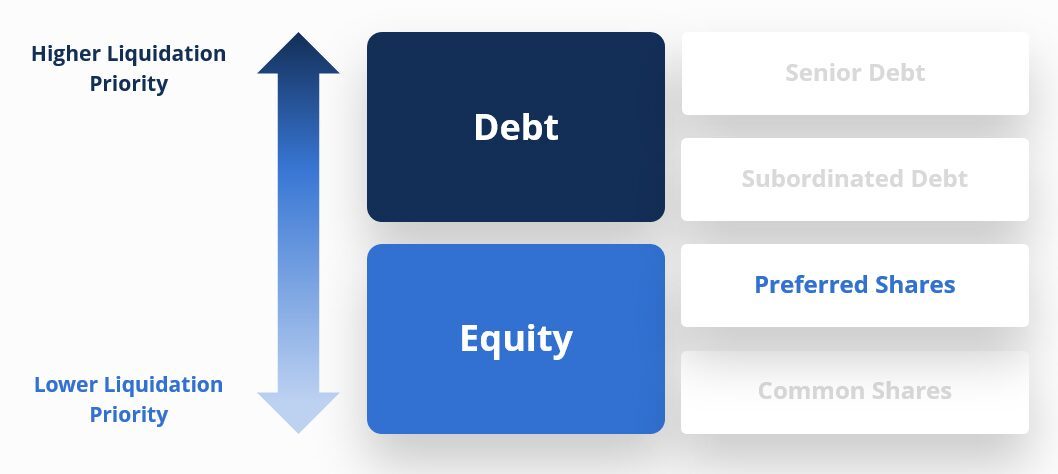

To understand the securities used by venture capital investors, it is important to understand the distinction between Debt and Equity.

From a business’ perspective:

The equity versus debt decision relies on a number of factors such as the current economic climate, the business’ existing capital structure, and the business’ life cycle stage, to name a few.

Venture capital investors are tasked with determining what securities are most fitting for a given company – either debt or equity instruments.

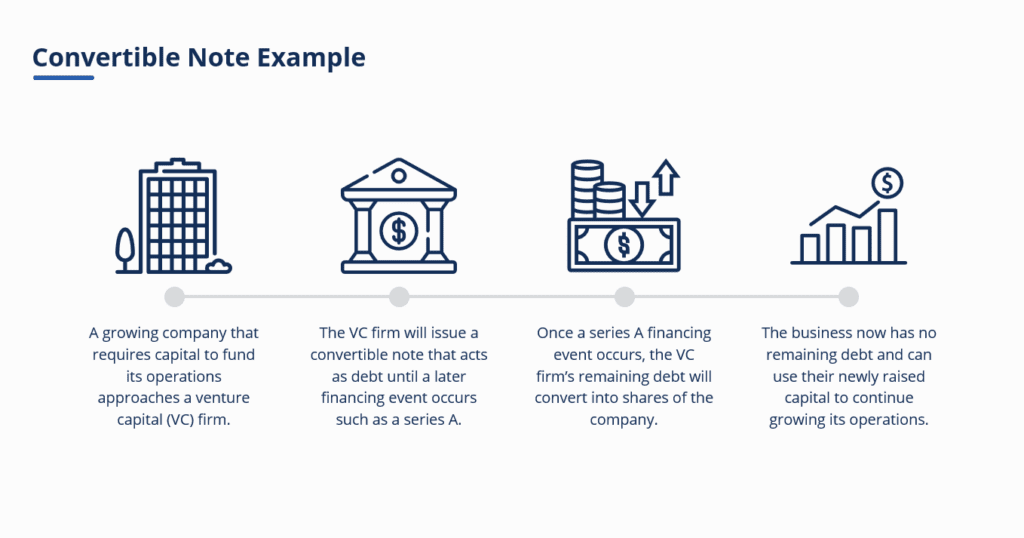

One of the most common instruments used by venture capital investors is convertible notes.

Convertible notes are short-term debt instruments designed to convert to equity at a predetermined conversion event, typically a future financing or liquidation event like an IPO (Initial Public offering) or acquisition. Furthermore, since convertible notes are loans, they also have a maturity date and an interest rate.

If a conversion event occurs in the future, the total amount converting into equity will include the original principal amount on the convertible note and any interest accrued to date. The price at which the convertible note converts to equity will be determined by one of the following:

Both valuation caps and discount rates allow noteholders to receive cheaper equity by converting at a discounted valuation. The result of this is that note holders end up with a larger percentage of the company than they otherwise would.

The better equity price helps compensate early investors for the higher amount of risk they take on by investing in the business earlier.

Convertible debt is used by investors because it is simple and can be issued quickly. Unlike other securities, investors and founders aren’t required to agree on a valuation of the business when negotiating the terms of a convertible note which is typically an intensive diligence process with high legal fees.

Additionally, since convertible notes are recorded as debt on the balance sheet up until the conversion event, The venture capital investor is going to have a senior liquidation preference if there is no future financing. This means that if the company exits at a lower amount than expected, the noteholders will be paid out before the equity investors.

A SAFE (Simple Agreement for Future Equity) is a kind of convertible security that allows note holders to purchase a specified number of shares for an agreed-upon price at some point in the future.

SAFE notes are similar to convertible notes in that they convert at a future financing event such as a series A. They also usually have a valuation cap or discount rate to give venture capital investors a favorable valuation when buying their equity.

The biggest difference between a convertible note and a SAFE note is that there is no debt component and, as a result, no interest rate or maturity date associated with the security.

SAFE notes were popularized by the now famous start-up accelerator Y-Combinator, which wanted access to a more founder-friendly security than convertible debt.

In addition to being advantageous to founders, SAFE notes are relatively easy to issue because no current company valuation is required, and there are fewer other components to the instrument that must be negotiated.

Preferred equity refers to a share class within a company’s shareholder equity. This kind of stock is commonly used by venture capital investors in later-stage deals and has a number of advantages in comparison to common shares.

The two main reasons venture capital investors would opt for preferred equity instead of common equity are: 1) its seniority to common shares, and 2) preferred equity may include negotiable provisions like additional voting rights and/or anti-dilution clauses.

Preferred shares are considered senior to common shares in the case of a liquidation or sale of the company. This means that if the company a VC firm has invested in is forced into a liquidation scenario (or it exits at a lower price than anticipated), owners of preferred shares will be paid out before common shareholders (although still behind creditors).

This limits the risk investors take on since there is a higher likelihood that they will be paid than if they owned common shares in the company, which fall at the bottom of the capital stack.

Owning preferred shares in a private company can also give investors voting rights that may be used to influence important strategic decisions. Venture capital investors will also often negotiate for the option to elect members to the board of directors to have more influence on the direction of the company.

A founder and their investors may have very different objectives with regard to a company or a project. The founder may be concerned with the process (i.e., the means), whereas the investor may only be concerned with their return (i.e., the end).

This can make discussions and general collaboration between founders and investors challenging as they may have conflicting objectives around how the company should be run.

Thank you for reading CFI’s guide to Venture Capital Financing. To keep advancing your career, the additional CFI resources below will be useful: